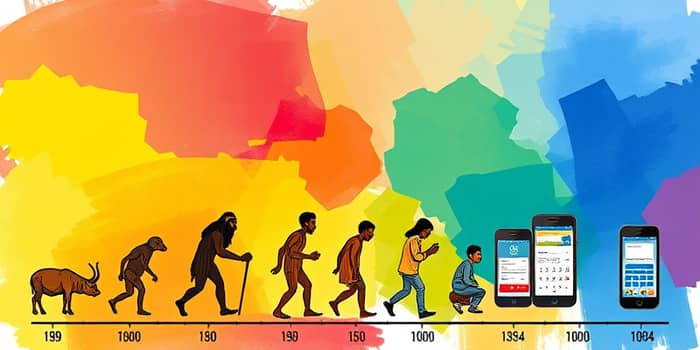

The story of global payments is a testament to human creativity and resilience, spanning millennia from simple trades to instant digital exchanges.

This evolution has been driven by the relentless pursuit of convenience and security, transforming economies and everyday life in profound ways.

By exploring this history, we can gain practical insights to navigate today's fast-paced financial world with confidence and inspiration.

Over 12,000 years ago, societies relied on the barter system for transactions.

Goods and services were exchanged directly, but this method had significant limitations.

As communities grew, the need for a more standardized medium became apparent.

Commodity money emerged, using items like shells, grains, and livestock as units of exchange.

This innovation laid the groundwork for more sophisticated financial systems.

During the Tang Dynasty in China, paper money was introduced, revolutionizing commerce.

Its lightweight portability made it easier to handle compared to heavy metal coins.

By the Song Dynasty, paper currency became widespread, setting a precedent for future innovations.

In Europe, banknotes and checks appeared in the 17th century, often issued by goldsmiths as receipts for stored gold.

Cheques, first recorded in 806 CE, allowed individuals to transfer money without physical cash, improving security.

These developments marked a shift towards more formalized and secure transaction methods.

The 19th century saw the introduction of Electronic Funds Transfer (EFT) in the 1870s.

Western Union debuted with "wire transfers," enabling electronic movement of money across distances.

Despite this, cash remained the dominant form of payment for most of history due to its anonymity and ease of use.

However, cash had limitations, including the need for physical handling and susceptibility to theft.

This era set the stage for the digital transformations to come.

In the 1950s, credit cards like Diners Club emerged, offering a secure and convenient alternative to cash.

By the end of 1950, Diners Club achieved considerable success, accepted at numerous restaurants.

Competitors like American Express and Bankamericard (later VISA) entered the market, expanding consumer options.

Debit cards were introduced in the 1970s, allowing direct payments from bank accounts without credit reliance.

Technology advances, such as magnetic stripes in 1969 and ATMs in 1967, enhanced card functionality.

RFID, chips, and contactless payments in the 1990s provided even more security and convenience.

The internet's arrival in the mid-1990s created new business models demanding innovative payment methods.

Payment gateways like PayPal, launched in 1998, revolutionized online shopping and e-commerce.

PayPal gained popularity after its acquisition by eBay in 2002, making digital wallets mainstream.

This digital boom offered consumers easier and more secure ways to shop online.

It also set the stage for the mobile revolution that followed.

The widespread adoption of smartphones in the 2010s led to the rise of mobile payments and digital wallets.

Apple Pay, Google Wallet, and Samsung Pay provided unprecedented convenience and security for users.

Open banking emerged in the mid-2010s as a transformative force, allowing direct payments from bank accounts.

Contactless payments, enabled by NFC technology, became increasingly popular, reducing physical contact and speeding up transactions.

This era emphasized user-centric design and real-time accessibility.

The 2020s have brought significant advances with cryptocurrencies and blockchain technology transforming the landscape.

Central Bank Digital Currencies (CBDCs) may become the norm, offering government-backed digital money.

The total transaction value of digital payments is projected to reach $16.59 trillion by 2028, highlighting rapid growth.

These developments promise to make payments even more seamless and inclusive globally.

Efficient settlement systems are crucial for modern payments, evolving from manual processes to real-time solutions.

In the mid-20th century, interbank payments in Switzerland could take up to four days to execute.

The introduction of Real-Time Gross Settlement (RTGS) systems, like Swiss Interbank Clearing in 1987, was a major milestone.

Retail payments are increasingly settled via these systems, ensuring faster and more reliable transactions.

The evolution of payments has been shaped by innovation, changing consumer needs, and technological advancements.

Fintechs have played a pivotal role in improving speed, convenience, and accessibility.

From barter to blockchain, the acceleration is remarkable; it took 9,500 years to reach paper money, but less than 60 years for nearly invisible payments.

Understanding this history inspires us to adapt and thrive in an ever-changing financial world.

By learning from the past, we can make informed choices that enhance our personal and professional lives.

References